Lindel Enticott

Lindel Enticott

.jpg?width=800&height=534&name=Adobe%20Express%20-%20file%20(6).jpg)

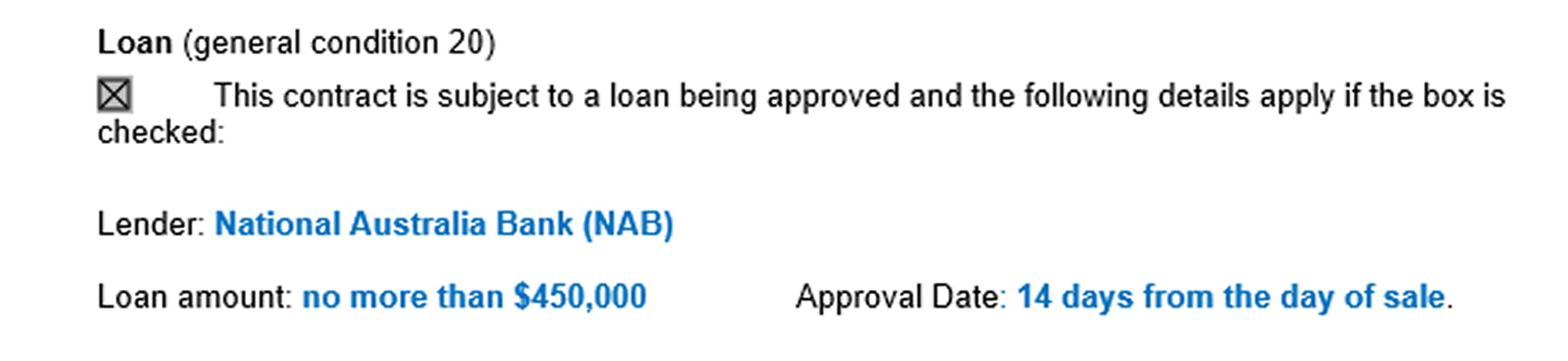

- The clause is included in the contract before signing

- You apply for finance immediately and due everything reasonable to obtain finance

- You give written notice before the approval date expires supported by suitable evidence

.jpg)

Understanding the statement of adjustments: What Victorian purchasers and vendors need to know before settlement

When buying or selling a property in Victoria, one conveyancing process that plays a crucial role in ensuring fairness and accuracy at settlement...